Venture Capital

Key Messages

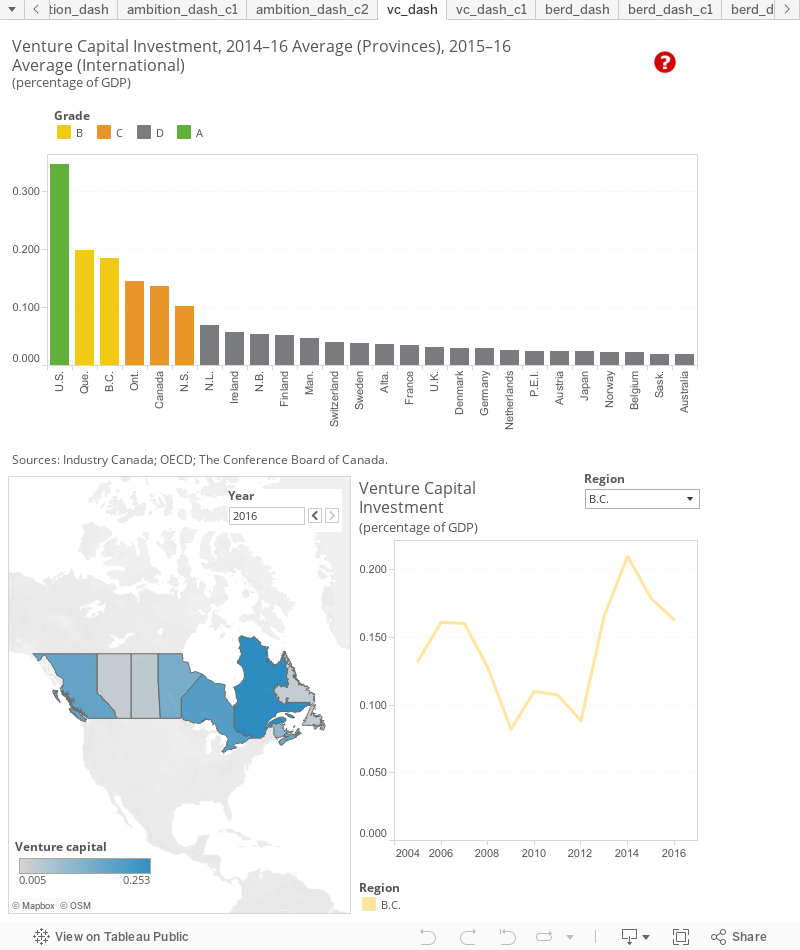

- Top-ranking provinces Quebec and B.C. both score B grades on venture capital investment, trailing the United States.

- While venture capital investment in Canada increases by more than 30 per cent since the previous report card, Canada falls from a B to a C grade because the United States has improved its performance substantially.

- Six provinces score D grades on venture capital investment.

Why is venture capital important to innovation?

Venture capital plays an important role in a region’s innovation ecosystem by providing emerging firms with early-stage financing—such as pre-seed, seed, start-up, and other early-stage funding—or later-stage financing—i.e., funding provided after commercial manufacturing but before an initial public offering.1 This risk capital provides firms with the financial resources they need to invest in further research and development, manufacturing, and marketing before they are able to generate solid revenue streams to do so on their own.

Venture capital is also an important source of managerial expertise—a key ingredient in successful innovation. Along with financing, venture capitalists bring entrepreneurial experience, industry knowledge, and networks of customers, suppliers, and other funders—all of which many new entrepreneurs lack. Given that Canada’s management capacity for innovation is weak relative to many international peers, this could be an important piece in solving Canada’s innovation puzzle.

What are some issues faced when comparing venture capital investment across countries?

Collecting comparable data on venture capital investment across countries is challenging, and some variability in performance may be a result of data issues rather than actual differences in performance. As the OECD notes, “there are no standard international definitions of venture capital nor of the breakdown of venture capital investments by stage of development. In addition, the methodology for data collection differs across countries. Data on venture capital are sourced from national or regional venture capital associations that produce them.”

The data used here are drawn from a “harmonized” OECD data set, as well as from Industry Canada’s Venture Capital Monitor, whose national- and provincial-level data align with the OECD dataset, and the Canadian Venture Capital Association.2

We use a two-year average for the international peers and a three-year average for the provinces to smooth out some of the year-to-year variability in venture capital investment, especially in smaller jurisdictions that see few deals. In smaller jurisdictions, one or two large venture capital deals in one year can make that jurisdiction look better at attracting venture capital than it really is on a long-term basis.

Consistent with the overall methodology for the innovation report card, changes in the provinces’ venture capital performance do not affect the grades assigned to countries. The countries’ grades are calculated relative to other countries only. Provincial grades are then determined using the grade thresholds generated by the countries’ performance. This is useful to mention given that Canada’s grade has slipped from a B to a C on venture capital—a result of the United States’ soaring performance and not movement by the provinces.

How does provincial performance on venture capital investment compare internationally?

Provincial performance varies widely. Fairly strong venture capital investment rates in Quebec (0.2 per cent of GDP) and B.C. (0.18 per cent) place those provinces second and third, respectively, among international jurisdictions—but far behind the United States, which has doubled its performance over the past two years (from 0.17 to 0.35 per cent). The United States earns an A, while Quebec and B.C. slip to B grades despite seeing stronger investment since the previous report card.

Ongoing investment in companies in the information and communications technology (ICT) and life sciences sectors has buoyed the venture capital investment rate in B.C. in recent years. Looking only at the most recent data for 2016 (rather than the three-year average), Quebec has shown bullish venture capital investment growth in the past five years—from 0.11 per cent of GDP in 2012 to 0.25 per cent of GDP in 2016.

Ontario-based firms received more venture capital money ($1.5 billion) than firms in other provinces in 2016, but Ontario’s venture capital investment rate as a percentage of GDP (0.15 per cent) is lower than that of the three leading jurisdictions and strong enough only for a grade of C.

Relatively high investment in Quebec, B.C., and Ontario combines to place Canada fifth overall—second among peer countries—but the country slips to a grade of C in light of the explosive performance of the United States in recent years.

Among the remaining provinces, Nova Scotia makes a leap from 10th to sixth among all jurisdictions and improves from a D to a C grade. Had the United States not performed so well, Nova Scotia would likely have earned a B. Newfoundland and Labrador maintains its ranking at seventh but falls from a C to a D grade.

All other provinces rank ninth or lower and earn D grades on this indicator. Unlike the previous report card, no province earns a D–, as Australia has fallen to the back of the class.

Analyzing the performance of the smaller provinces presents a challenge given the volatile nature of venture capital investment. For example, although Newfoundland and Labrador had an average venture capital investment rate of 0.07 per cent of GDP between 2014 and 2016, this was largely the result of only 10 venture capital deals totalling $10 million in 2015 and 2016, while nominal GDP (the denominator for the indicator) fell in the province.

Venture capital investment in Canada overall has increased substantially in recent years—from $1.5 billion (0.09 per cent of GDP) in 2011 to over $3.2 billion (0.16 per cent of GDP) in 2016. Canada’s three-year average venture capital investment rate sits at 0.14 per cent of GDP. Meanwhile, most of Canada’s global peers have not recovered from massive declines in venture capital investment as a percentage of GDP from 2009 to 2014. As a country, Canada climbed from third-worst in 2009 to second-best in venture capital investment among 16 peer countries in 2014, where it remains today. Yet Canada’s performance pales in comparison to what the United States has experienced in recent years.

How do the provinces fare relative to one another?

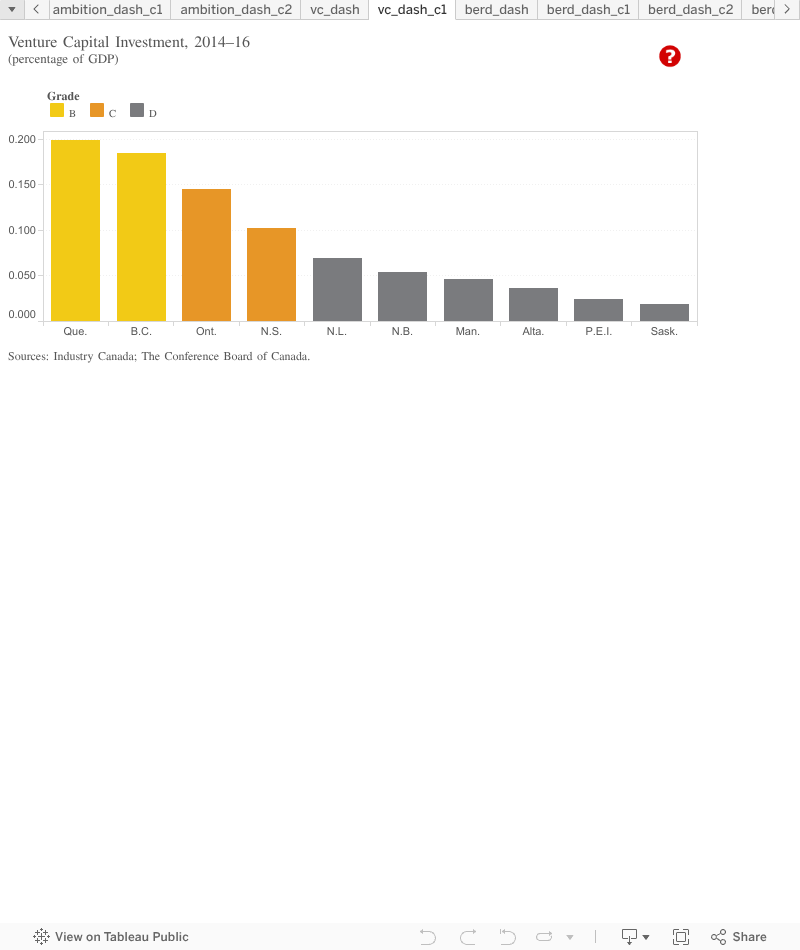

Quebec and B.C. are the highest-ranked provinces and the only two B performers on venture capital investment, while P.E.I and Saskatchewan are the lowest-ranked provinces, scoring D grades. Ontario and Nova Scotia earn C grades for venture capital investment of 0.15 and 0.1 per cent of GDP, respectively. Despite receiving a C grade, Nova Scotia has had impressive venture capital activity in recent years. In 2014, Nova Scotia recorded only nine deals for a total of $11 million in venture capital investment, but in 2016, firms in the province closed 22 deals worth $64 million.

Newfoundland and Labrador scores a D for venture capital investment of 0.07 per cent of GDP in 2014–16. Yet the rolling average masks a substantial decline from its peak of 0.17 per cent in 2014 (owing to two large deals totalling $60 million) to just 0.02 per cent based on four deals totalling only $7 million in 2016. Alberta has also had substantially lower venture capital investment—falling from $218 million in 2014 to $68 million in 2016, and slipping from 11th to 14th in the rankings.

Meanwhile, New Brunswick’s venture capital investment increased from $14 million in 2014 to $32 million in 2016, improving its ranking from 18th to an impressive ninth among all jurisdictions.

Are more Canadian firms receiving funding and management advice?

Overall, yes. The number of Canadian firms receiving venture capital—and thus management expertise and networks—climbed from 378 in 2009 to 530 in 2016. As with investment itself, there is variation across provinces: the number of deals is up in eight provinces and down or the same in two provinces. Ontario, New Brunswick, and Nova Scotia have experienced strong growth in companies receiving funding and management advice, while Quebec has seen a substantial decline in the number of firms receiving funding (despite the overall amount of funding nearly doubling from $532 million in 2011 and to $1 billion in 2016).

Whether these specific companies succeed or fail, the increase in entrepreneurs receiving real-world management guidance bodes well for Canada’s innovation performance in the future.

Number of Canadian Firms Receiving Venture Capital Has Increased, but Varies by Province

| Province | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

| B.C. | 48 | 52 | 52 | 57 | 51 | 60 | 86 | 71 |

| Alta. | 21 | 22 | 23 | 19 | 26 | 27 | 18 | 22 |

| Sask. | 10 | 5 | 8 | 12 | 4 | 4 | 3 | 11 |

| Man. | 6 | 8 | 5 | 6 | 1 | 1 | 3 | 6 |

| Ont. | 103 | 117 | 132 | 152 | 139 | 142 | 206 | 200 |

| Que. | 172 | 192 | 217 | 169 | 154 | 151 | 168 | 164 |

| N.B. | 6 | 7 | 9 | 10 | 14 | 19 | 17 | 29 |

| N.S. | 9 | 6 | 8 | 18 | 12 | 9 | 27 | 22 |

| P.E.I. | 0 | 0 | 0 | 0 | 0 | 1 | 2 | 1 |

| N.L. | 3 | 0 | 0 | 3 | 1 | 2 | 6 | 4 |

| TOTAL | 378 | 409 | 454 | 446 | 402 | 416 | 536 | 530 |

Source: The Conference Board of Canada.

Is most venture capital funding for Canadian firms early-stage or late-stage?

In 2016, Canada’s mix of early-stage and late-stage venture capital funding moved closer to the norm among international peers than it was in 2013. Roughly 56 per cent of venture capital investment in Canada in 2016 took the form of early-stage financing—i.e., pre-seed, seed, and start-up funding—versus an average of 62 per cent among international peers. The other 44 per cent of Canada’s venture capital in 2016 was later-stage financing. In 2013, Canada’s early-stage financing accounted for just 20 per cent of venture capital investment. The 2016 distribution brings Canada close to its 2009 pattern, when early- and later-stage venture capital investments were roughly equal and more in line with the global norm.

The reasons for the uniquely Canadian shift toward later-stage funding in 2013 are not clear. Nevertheless, the return to roughly equal shares of early- and late-stage financing, along with substantial growth in total funding, reflects a financing environment more suited to supporting companies at all stages.

Has provincial performance on venture capital investment improved over time?

Many provinces are performing much better now than they were five years ago. Among larger provinces, total investment has nearly tripled in Ontario since 2011 and nearly doubled in Quebec and British Columbia. Among smaller provinces, Saskatchewan, New Brunswick, and Nova Scotia have seen total investment rise since 2011, although year-to-year volatility is evident. At $90 million in 2016, Manitoba witnessed its largest venture capital investment in more than 10 years. However, the number of annual deals remains relatively low, which suggests that the 2016 result may be an anomaly.

In Alberta, the number of firms receiving funding remained relatively steady from 2011 to 2016, and total investment hit a high of $213 million in 2014. But by 2016, following the collapse in the price of oil, Alberta saw its lowest venture capital investment ($68 million) in nearly a decade. Investment in P.E.I. and in Newfoundland and Labrador varies substantially from year to year.

How has Canada vaulted from being one of the worst to one of the best performers in recent years?

Between 2009 and 2013, venture capital investment rates declined in every peer country except Canada and the United States, where they increased by 61 per cent and 96 per cent, respectively. That resulted in Canada vaulting itself from being one of the worst to one of the best performers on this indicator in just a few years. In the past three years, Canada and many provinces have had continued steady growth in venture capital. This appears to be a result of a few factors:3

- Venture capital investment tends to follow the business cycle and has grown along with gradual improvement in Canada’s economy since the recession. Although venture capital investment in Canada grew from just under $1 billion to more than $2.3 billion between 2009 and 2014, that simply brought it to its pre-recession level of $2.3 billion in 2007. Since 2014, total investment has leaped to $3.2 billion.

- In 2013, the federal government’s Venture Capital Action Plan committed $400 million to venture capital funds and sought to raise another $800 million from outside investors. That investment is clearly contributing to growth, along with investment from other sources in the Canadian and global venture capital ecosystem.

- Finally, U.S.-based venture capital investment in Canada continues to play a role. Historically, roughly 30 per cent of venture capital investment in Canada has been funded by foreign, primarily U.S.-based, sources. By 2014, U.S. sources alone accounted for over 37 per cent of the $1.9-billion venture capital investment in Canada whose sources were known.

Overall, Canada has maintained a strong growth trajectory in venture capital investment, but its neighbour to the south has had substantially stronger gains. In the U.S., venture capital investment as a share of GDP doubled from 0.17 per cent in 2014 to 0.35 per cent by 2016. Although Canada’s track record is impressive, there is clearly much more money available for start-up and growth for firms in the United States—which means that Canadian firms operating in North American markets may struggle to find the resources to compete with American competitors. Indeed, it is wise to remember that although the venture capital scene is healthier in Canada than in Europe, Canadian firms face a significant disadvantage relative to their closest competitor firms in the United States.

How can provinces improve and sustain venture capital strength?

At the moment, performance in three of Canada’s largest provinces is relatively strong, while in the other provinces it ranges from fair to poor. As firms in the United States attract unprecedented levels of venture capital, the relative performance of Canada and its leading provinces is beginning to erode. Performance has improved for some Canadian jurisdictions, but further improvements are needed.

For any jurisdiction to do well in venture capital investment—and, in turn, reap the innovation benefits of venture capital investment—it needs three things: people or organizations with money to invest, firms worth investing in, and mechanisms to link the two groups.

- There is a large pool of potential capital from which to draw in Canada, but much of it has been invested in low-risk sectors with proven track records. Investment in higher-risk ventures is limited in Canada partly due to insufficient information and expertise among investors. The Conference Board has noted that “Canada has enough institutional funders and high-net-worth individuals to improve the depth and breadth of Canada’s risk capital, if they choose to become more engaged…. [But] there is a need to improve the Canadian risk capital industry’s track record for selecting deals and earning returns. Tracking and publishing deal information will help the market make better-informed risk capital decisions.”4

- At the same time, venture capital investment will grow only if Canadian firms that are worthy of venture capital investment continue to emerge. Many Canadians with good ideas are starting businesses and looking for capital. But few have the managerial capacity to commercialize, grow, and make a good case to potential financiers that their businesses are worthy of investment. Building managerial capacity and providing guidance to entrepreneurs seeking funding will be critical in sustaining and improving venture capital strength in the provinces.5

- Finally, even where there are worthy firms and willing investors, the Canadian market is so large and fragmented that the two groups have difficulty finding each other. Another area for action is in developing better mechanisms and tools to link entrepreneurs with venture capital. In addition to further supporting initiatives and institutions that connect entrepreneurs and investors, such as Startup Canada, Communitech, and MaRS Discovery, Canada could “develop more managers, lawyers, accountants, analysts, and brokers who specialize in the unique challenges facing start-up companies. These intermediaries are key to both extending the competencies of start-up companies and linking start-up entrepreneurs with risk capital providers.”6

Footnotes

1 OECD, Entrepreneurship at a Glance 2014 (Paris: OECD, 2014), 22.

2 Ibid., 22, 102–4; Industry Canada, Venture Capital Monitor; Canadian Venture Capital Association, VC & PE Canadian Market Overview (Toronto: CVCA, 2016).

3 Daniel Munro, Canada’s Venture Capital Opportunity (Ottawa: The Conference Board of Canada, 2015).

4 Michael Grant, Start Me Up: Funding Canada’s Emerging Innovators (Ottawa: The Conference Board of Canada, 2014), 72–3.

5 Ibid., 72.

6 Ibid., 74.